"It is difficult to free fools from the chains they revere."

-- Voltaire

*********************************

Have you ever heard of a wage slave?Stop lying… of course you have...

Even worse... are YOU a wage slave?

Wage slaves are hidden in plain sight.

And they're everywhere.

They live in big houses.

They drive fancy cars.

They drive fancy cars.

They wear stylish [expensive] clothes.

But appearances are deceiving. They have more "things" than they have financial liquidity. In fact, they're collection of things are often collected by going into debt.

But appearances are deceiving. They have more "things" than they have financial liquidity. In fact, they're collection of things are often collected by going into debt.

They’re what’s known as “Ghetto Rich.”

It doesn't matter how "rich" you look... If you can't walk away from your job -- even for a second -- because you would no longer be able to pay the bills, you're a wage slave. And being a wage slave has leveraged and long term impacts.

It doesn't matter how "rich" you look... If you can't walk away from your job -- even for a second -- because you would no longer be able to pay the bills, you're a wage slave. And being a wage slave has leveraged and long term impacts.

The Retirement Problem

Most people want to retire at some point.

Some people even want to retire early.

Others just want a short-term retirement to enjoy their kids, travel and/or simply smell the roses for a bit.

Regardless of the "why," the problem is usually the "how." How do you pay your bills without that paycheck coming in each month? How do you build a nest egg that will allow you to smell those roses for a bit at some point. How do you escape wage slavery?

Here are 3 steps to get you started on the journey from “here to there…”

First, you need to change your thinking from high wages to high positive cashflow.

Third, your assets must generate enough return to support the future that you want for yourself and your family. The required return comes in many different forms. Interest payments on cash balances and securities, capital gains on securities, cashflow from assets like rental properties, dividends from securities, etc.

Sounds easy enough, right?

That’s the old “find the next Microsoft” attitude from many years ago.

Stop right now. You're heading down the wrong path. Not to mention embarrassing yourself.

If your plan is to double or triple your money by using any number of get-rich-quick schemes -- hot IPOs, penny stocks, stocks that grow to the moon, real estate flipping, excessive leverage -- I'm here to tell you that it won’t happen.

Ever.

Similarly, if you think you’re going to get there with your high wage job and plain vanilla “investing,” I can promise you, you’ll be immensely disappointed.

And that disappointment will happen at the absolute worst time possible… when you’re too old to do anything about it.

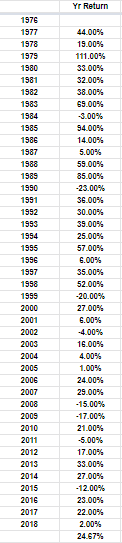

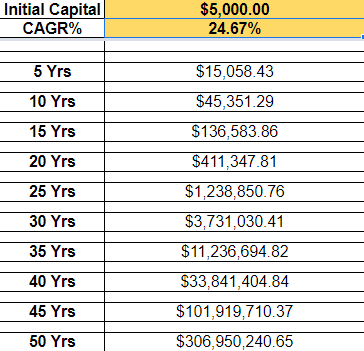

Warren Buffett, the most famous and successful investor of all time, spends all day every day thinking about what he's going to invest in next (he actually doesn’t but let’s pretend he does for the sake of this little piece). For all his efforts, his investment vehicle Berkshire Hathaway realized an average annual return of 24.67% beginning in 1976 thru 2018.

That’s not bad as over a long enough period, that would generate a pretty hefty result.

The problem?

Most of us don’t have a spare 25 or 30 years laying around... to say nothing of 50.

Plus, do you have some reason to think based on your trading performance to this point that you can produce results like the "Oracle of Omaha?"

Plus plus, keep in mind ol’ Warren has a helluva sidehustle in the form of a big insurance business that throws off enormous cashflow each year via premiums that must be invested.

What’s my point?

Pretty simple actually. You can’t beat the pros at their game playing by rules designed at least in part to keep them out front.

So stop beating yourself up about it.

Step away from the ledge and examine the other elements of wealth creation before you jump.

But there's another way to look at it: A financially independent person can live on the income generated by her cashflow vehicles.

Semantics right?

Actually, it’s a difference in perspective.

The first point of view focuses almost solely on the amount of cashflow coming in -- a difficult endeavor to control… certainly at the beginning of approaching things this way.

The second point of view focuses on spending -- a variable that is very simple to control. Not necessarily easy, but simple enough.

And you know how I feel about simple.

The #1 reason people stay in wage slavery is that they spend too much.

Allow me to say that again...

The #1 reason people stay in wage slavery is that they spend too much.

Too much on housing...

Too much on cars...

Too much on entertainment/vacations...

Just too much.

The truth is the best way to achieve FI focuses on growing cashflow while simultaneously reducing/controlling spending.

Assuming you have truly retired, you’ll need your assets to support you. To generate $10,000 in cashflow, you need $200,000 to throw off 5% a year, every year. Congratulations -- your assets are now paying you enough to live on! You no longer need a salary because you've achieved financial independence. Get ready to hand your boss that letter of resignation.

But remember, to maintain financial independence, you need your wealth to keep generating about 5% a year, year in and year out. Small variations in cashflow will even out over time, but you'll need to avoid really massive swings -- especially massive swings lower.

The problem? You have built and now rely on an approach with limited visibility re what your process will actually throw off each year.

Being reckless and chasing "the next big thing" isn’t the answer either… It’s as close as you can get to a surefire way to kill your golden goose. Filling your portfolio with risky, temperamental investments that you don't have time to babysit is like throwing money down the toilet... and a stinky, public toilet at that.

A better alternative: Only have assets that yield a minimum of 5% in that $200k portfolio. Dividend paying stocks… coupon paying bonds… That’s a reasonable approach to achieve that fancy $10k per year… into perpetuity.

The best alternative: Learn a simple trading process that can throw off 8-12% per month consistently… by taking advantage of market volatility over smaller time frames via swing and/or day trading.

Some people even want to retire early.

Others just want a short-term retirement to enjoy their kids, travel and/or simply smell the roses for a bit.

Regardless of the "why," the problem is usually the "how." How do you pay your bills without that paycheck coming in each month? How do you build a nest egg that will allow you to smell those roses for a bit at some point. How do you escape wage slavery?

Here are 3 steps to get you started on the journey from “here to there…”

First, you need to change your thinking from high wages to high positive cashflow.

What’s the difference you say?

Wages are just that… they usually flow from a solitary source and are completely controlled by someone else.

Let me repeat... wages are your revenue channel that's completely controlled by someone else.

Cashflow on the other hand, can and often does, come from multiple channels... profits from sidehustles for example. More important, you have more control and the ability to grow cashflow than wages. That becomes enormously important as you move forward and use up that other precious resource... Time.

Second, you need to bring your spending under control. If you can't (or won't), you will never be financially independent. The moment that your spending is consistently inside your independent cashflow (cashflow beyond your wages), you’re technically financially free.

Second, you need to bring your spending under control. If you can't (or won't), you will never be financially independent. The moment that your spending is consistently inside your independent cashflow (cashflow beyond your wages), you’re technically financially free.

Third, your assets must generate enough return to support the future that you want for yourself and your family. The required return comes in many different forms. Interest payments on cash balances and securities, capital gains on securities, cashflow from assets like rental properties, dividends from securities, etc.

Sounds easy enough, right?

The World's Worst Investing Idea

If you're like most "investors," you probably live with the mantra, "All I need to do is find a few high-flying investments that supercharge my net worth, then I'll be able to retire."That’s the old “find the next Microsoft” attitude from many years ago.

Stop right now. You're heading down the wrong path. Not to mention embarrassing yourself.

If your plan is to double or triple your money by using any number of get-rich-quick schemes -- hot IPOs, penny stocks, stocks that grow to the moon, real estate flipping, excessive leverage -- I'm here to tell you that it won’t happen.

Ever.

Similarly, if you think you’re going to get there with your high wage job and plain vanilla “investing,” I can promise you, you’ll be immensely disappointed.

And that disappointment will happen at the absolute worst time possible… when you’re too old to do anything about it.

Warren Buffett, the most famous and successful investor of all time, spends all day every day thinking about what he's going to invest in next (he actually doesn’t but let’s pretend he does for the sake of this little piece). For all his efforts, his investment vehicle Berkshire Hathaway realized an average annual return of 24.67% beginning in 1976 thru 2018.

That’s not bad as over a long enough period, that would generate a pretty hefty result.

The problem?

Most of us don’t have a spare 25 or 30 years laying around... to say nothing of 50.

Plus, do you have some reason to think based on your trading performance to this point that you can produce results like the "Oracle of Omaha?"

Plus plus, keep in mind ol’ Warren has a helluva sidehustle in the form of a big insurance business that throws off enormous cashflow each year via premiums that must be invested.

What’s my point?

Pretty simple actually. You can’t beat the pros at their game playing by rules designed at least in part to keep them out front.

So stop beating yourself up about it.

Step away from the ledge and examine the other elements of wealth creation before you jump.

You can achieve your goal of financial independence -- you just have to tackle it from a different angle and with different means.

The Fast Track to Financial Independence

A financially independent person's cashflow delivers enough income to live on. I think maybe I said that above…But there's another way to look at it: A financially independent person can live on the income generated by her cashflow vehicles.

Semantics right?

Actually, it’s a difference in perspective.

The first point of view focuses almost solely on the amount of cashflow coming in -- a difficult endeavor to control… certainly at the beginning of approaching things this way.

The second point of view focuses on spending -- a variable that is very simple to control. Not necessarily easy, but simple enough.

And you know how I feel about simple.

The #1 reason people stay in wage slavery is that they spend too much.

Allow me to say that again...

The #1 reason people stay in wage slavery is that they spend too much.

Too much on housing...

Too much on cars...

Too much on entertainment/vacations...

Just too much.

The truth is the best way to achieve FI focuses on growing cashflow while simultaneously reducing/controlling spending.

Since I spend most of my writing focused on asset (account) growth, I’ll spend the balance of this post talking about the other side of the equation.

Your savings rate is the percentage of your total cashflow you're able to save, assuming that you need the rest of the income to pay the bills. And if you aren't willing to save more than you spend, I can assure you that it will be hard [ie damned near impossible] to achieve financial independence.

The beauty of focusing on your savings rate? There's zero risk involved. Anyone willing to make the lifestyle changes to achieve a high savings rate can easily enhance their ability to retire earlier than expected... or retire at all these days.

To find out how soon you could retire, let's try a simple formula.

Assume you have cashflow of $50,000 a year. But you've cut your expenses by so much that you only need $20,000 a year to live comfortably. Your savings rate is ($50,000 - $20,000) / $50,000 = 60%.

Once you have your savings rate figured out, you can use this next formula to calculate how long it will take you to achieve financial independence:

Assuming a 5% return on investment (really? Here’s another place to be embarrassed… I make 5% by mistake... but we’ll talk more about that in a different post), post-taxes, you can achieve financial freedom in:

Neither can I…

But I chose that extreme level of saving to illustrate the ridiculous nature of some of the more extreme F.I.R.E. (Financial Independence Retire Early) folks.

And by the way… who the hell can retire on a little over $200,000? That’s the amount you’d be left to live on after 5 years of saving 80% of your $50,000 income.

Oh, wait… the whole F.I.R.E. approach assumes that you’ll continue to live under the same level of austerity in retirement as that which allowed you to achieve retirement in the first place.

Sounds like fun.

Lest you think me stuck on stupid like so many gurus preaching this garbage, let me throw a couple of thoughts out.

First, by converting to independent cashflow, your income doesn’t necessarily start taking a hit the day you retire.

Second, if you are constantly increasing said independent cashflow, your retirement prospects (in terms of standard of living) only get better.

The point is, regardless of how far you're willing to take it, knowing that anyone can achieve financial independence in a very short amount of time is powerful stuff. And while your savings rate, i.e. your lifestyle, is intimately intertwined with your ability to become financially independent when you want, so too is your ability to create independent cashflow for yourself.

Your savings rate is the percentage of your total cashflow you're able to save, assuming that you need the rest of the income to pay the bills. And if you aren't willing to save more than you spend, I can assure you that it will be hard [ie damned near impossible] to achieve financial independence.

The beauty of focusing on your savings rate? There's zero risk involved. Anyone willing to make the lifestyle changes to achieve a high savings rate can easily enhance their ability to retire earlier than expected... or retire at all these days.

To find out how soon you could retire, let's try a simple formula.

Assume you have cashflow of $50,000 a year. But you've cut your expenses by so much that you only need $20,000 a year to live comfortably. Your savings rate is ($50,000 - $20,000) / $50,000 = 60%.

Once you have your savings rate figured out, you can use this next formula to calculate how long it will take you to achieve financial independence:

Assuming a 5% return on investment (really? Here’s another place to be embarrassed… I make 5% by mistake... but we’ll talk more about that in a different post), post-taxes, you can achieve financial freedom in:

- 13.3 years if you save 60% of your cashflow;

- 8.6 years if you save 70% of your cashflow; and

- 5 years if you save 80% of your cashflow

Neither can I…

But I chose that extreme level of saving to illustrate the ridiculous nature of some of the more extreme F.I.R.E. (Financial Independence Retire Early) folks.

And by the way… who the hell can retire on a little over $200,000? That’s the amount you’d be left to live on after 5 years of saving 80% of your $50,000 income.

Oh, wait… the whole F.I.R.E. approach assumes that you’ll continue to live under the same level of austerity in retirement as that which allowed you to achieve retirement in the first place.

Sounds like fun.

Lest you think me stuck on stupid like so many gurus preaching this garbage, let me throw a couple of thoughts out.

First, by converting to independent cashflow, your income doesn’t necessarily start taking a hit the day you retire.

Second, if you are constantly increasing said independent cashflow, your retirement prospects (in terms of standard of living) only get better.

The point is, regardless of how far you're willing to take it, knowing that anyone can achieve financial independence in a very short amount of time is powerful stuff. And while your savings rate, i.e. your lifestyle, is intimately intertwined with your ability to become financially independent when you want, so too is your ability to create independent cashflow for yourself.

Making Sure Your Cashflow Can Keep Up

After all that hard work of boosting your savings rate to build your wealth, you don't want to let the way you handle your savings and assets to let you down once you need the cashflow. Let's go back to our example to see why.Assuming you have truly retired, you’ll need your assets to support you. To generate $10,000 in cashflow, you need $200,000 to throw off 5% a year, every year. Congratulations -- your assets are now paying you enough to live on! You no longer need a salary because you've achieved financial independence. Get ready to hand your boss that letter of resignation.

But remember, to maintain financial independence, you need your wealth to keep generating about 5% a year, year in and year out. Small variations in cashflow will even out over time, but you'll need to avoid really massive swings -- especially massive swings lower.

The problem? You have built and now rely on an approach with limited visibility re what your process will actually throw off each year.

Being reckless and chasing "the next big thing" isn’t the answer either… It’s as close as you can get to a surefire way to kill your golden goose. Filling your portfolio with risky, temperamental investments that you don't have time to babysit is like throwing money down the toilet... and a stinky, public toilet at that.

A better alternative: Only have assets that yield a minimum of 5% in that $200k portfolio. Dividend paying stocks… coupon paying bonds… That’s a reasonable approach to achieve that fancy $10k per year… into perpetuity.

The best alternative: Learn a simple trading process that can throw off 8-12% per month consistently… by taking advantage of market volatility over smaller time frames via swing and/or day trading.

The Rub

If you want to reach financial independence quickly, you need a plan. Luckily, the plan only has two steps. First, get your lifestyle under control.

Second, focus on finding the best trading process for generating those powerful, consistent streams of cashflow over the long-run.

Second, focus on finding the best trading process for generating those powerful, consistent streams of cashflow over the long-run.

See? Simple.

There are lots of places to learn this approach. In fact, I have a process of my very own. But this is not a sales piece, so you won’t find links to it here.

But if you really want to find it, I’m sure you can find a way😆.

There are lots of places to learn this approach. In fact, I have a process of my very own. But this is not a sales piece, so you won’t find links to it here.

But if you really want to find it, I’m sure you can find a way😆.

======================

======================

You Might Also Like: